Real Estate

Dubai D33: Agenda Of Growth – Market Overview, Long-Term Outlook

Property prices have surged in Dubai, fuelled by intense demand for a variety of reasons. The author of this article examines the state of the market, and what the future holds.

The following article about the Dubai real estate market comes from Christian Atzert. Atzert has been engaged in the Dubai property market since 2005 as an independent consultant, advising institutional and private clients on asset acquisitions, legal structuring as well as property management matters. He heads Dubai-based PPP Advisors.

The editors of this news service are pleased to share these comments; the usual disclaimers apply about views of outside contributors. To jump into the debate, email tom.burroughes@wealthbriefing.com

Property prices in the Dubai market have increased substantially over the last three years, prompting some commentators to frivolously announce the onset of a new bubble.

However, a spectacular GDP growth of 7.6 per cent in 2022 paired with continued significant inflows of people and investment capital may lead to other conclusions.

This article therefore aims to put the current market metrics into a broader perspective and present an outlook on the long-term developments, specifically in light of Dubai`s goals announced under the D33 development strategy.

Relief rally followed sell-off

Firstly, it is noteworthy that the present property cycle has

started out from an extremely low baseline, following six years

of gradually receding valuations, further exacerbated by a panic

sell-off at the onset of Covid-19.

Intense demand for prime property has pushed prices in the luxury segment upward by 112 per cent since January 2020. While this may seem alarming at first glance, Dubai`s prime residential property is far from expensive compared with its peers.

According to Knight Frank et al, Dubai is the 16th most affordable luxury market in the world at present. Dubai prime residential properties cost an average of $9.470 per square metre, only around a third of the prices demanded in London, New York or Singapore.

Plan D33 – Dubai`s quest to rise to the

top

Plan D33, a Dubai government roadmap and economic plan recently

unveiled is geared at – inter alia – establishing Dubai

within the top four of the world`s leading financial hubs

(presently number 22) alongside London, New York and Singapore by

the year 2033.

Besides aiming to become a top dog in financial centres, Plan D33

entails further targets with respect to Dubai`s economic

performance:

- increase foreign direct investment (FDI) to $16.3 billion

per annum (+87 per cent);

- increase its foreign trade to $7 trillion (+80 per cent,

decade on decade); and

- increase gross domestic product (GDP) by 36 per cent

decade on decade.

While this undertaking may seem ambitious at first, Dubai has an impressive track record of achieving similar feats.

Top-tier banks, family offices, hedge funds and other big players within the financial realm are already setting up shop in Dubai, the continuation of which will inevitably further nourish the immigration of high-profile employees, entrepreneurs and investors catering to and feeding off the financial ecosystem.

PPP Advisors strongly believe that (luxury) property valuations in Dubai will – during the course of this process – further converge with those seen in other leading financial hubs.

Relative value compared with peer cities

Meanwhile, luxury property in Dubai is presently valued at 33 per

cent less compared with such assets in Berlin, Germany`s capital

which is already placed in the lower third of the ranking for the

world`s most expensive cities.

Considering a shortage of prime residential property under construction in Dubai and a continued strong demand, the firm expects the upward trajectory to remain intact for the foreseeable future, albeit at a slower pace.

With prime waterfront properties such as Palm Jumeirah and

Jumeirah Bay being limited, we see a trickling down/diversion of

prime property demand into inland high-end communities such as

Jumeirah Islands, Jumeirah Golf Estates, Tilal al Ghaf and Al

Barari.

Common denominators amongst the former are modern, high-quality

apartments and villas with ample living spaces, top-notch

community services and infrastructure complemented by excellent

connectivity.

Off plan vs secondary market – no signs

of overheating

We have stated previously and the presently available transaction

data proves that Dubai`s third market cycle is characterised by a

dominance in real demand of end users and second-home

buyers.

This was profoundly different in 2009, on the eve of the global financial crisis and preceding the stark correction in Dubai`s property market. At that time, the off-plan segment was dominating secondary market transactions, representing 61 per cent of all property sales. Whereas development activity has indeed picked up in the recent years on the back of returning demand and the influx of expats, 2022 saw a proportion of only 44 per cent of off-plan sales against 54 per cent in secondary market transactions, a figure in line with the 10-year average.

Stability as a new paradigm

Without a doubt, however, the dominance of real property demand

and its stability is a rather new phenomenon in Dubai`s

marketplace.

While Dubai had been experiencing a series of economic cycles characterised by high volatility in population, economic output and – in turn – property prices, the Emirate`s policies with respect to visa and company ownership regulations seem to have fundamentally transformed the demand metrics.

Further supported by a more stable political environment in the greater MENA region and combined with political and economic turmoil in European and other First World countries, expats are more likely to call Dubai their home for much longer than before, if not until retirement or even beyond.

At the same time, a number of factors such as Dubai`s early reopening after the pandemic and the UAE`s progressing integration into the BRICS group of countries is likely to have attracted a sizeable number of new investors and immigrants from practically new source markets, namely the US and Canada.

Remarkably, but certainly due to the factors mentioned above, Dubai has not seen a slowdown in economic activity like the European and North American economies.

As a result, Dubai`s real estate market is increasingly exhibiting characteristics of a mature market, showing stability in demand and supply, leading to a higher resilience against exogenous shocks (i.e. rising interest rates).

International survey amongst HNW individuals with

remarkable results

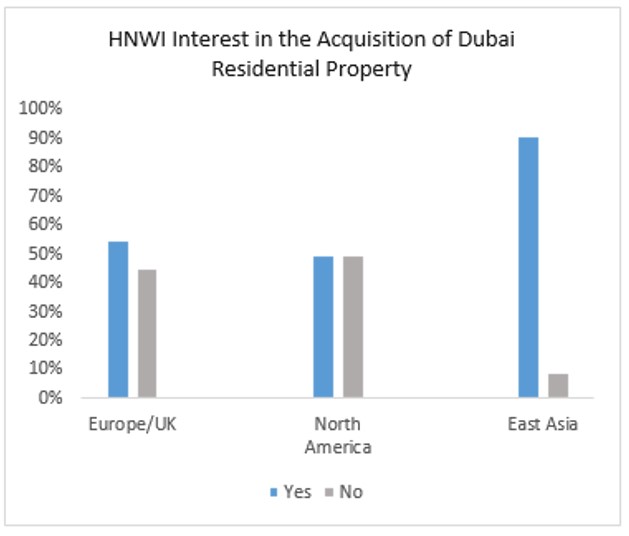

A worldwide survey, recently conducted by Knight Frank amongst

high net worth individuals, has prompted some eye-opening

insights into the strong appetite for Dubai properties within

this cash-rich clientele.

Specifically, 90 per cent of the respondents from East Asia have expressed an interest in investing into residential property in Dubai while their peers from Europe/the UK (55 per cent) as well as North America (50 per cent) have also exhibited a strong appetite for Dubai properties. Some 40 per cent of the HNW individuals stated that their purchase would be purely for personal or second-home use while 60 per cent would see their acquisition as an investment. It is an obvious assumption and noteworthy therefore that a substantial percentage of properties purchased by this buyers' group would not be made available in Dubai`s rental market.

We have reason to believe that the tendency of a weaker US dollar will increase the budgets (denominated in dollar/Dirham) and possibly accelerate the decision-making of investors towards their property acquisition within the Asian and European jurisdictions, thereby driving more capital into the Dubai market.

Conclusion

On the back of forward-looking policymaking by the government

combined with favourable geopolitical shifts and notably a weaker

dollar, Dubai`s growth is accelerating, progressing on its path

to evolve into one of the world`s leading business, finance and

tourism hubs.

Despite the recent price hikes, we see substantial further upwards potential if Dubai`s game plan is to play out over the course of the coming decade.

Moreover, as properties in tier-2 locations and qualities have only undergone a fraction of the price appreciation compared with the high-end segment, we see significant investment opportunities to be seized by smart investors.

To contact the author, email c.atzert@ppp-advisors.com