Practice Strategies

Meet The "Venture-As-A-Service" Funding Model

Professional investing structure and practices are arriving at the venture asset class, the author, a practitioner in the space, argues.

How should certain types of entrepreneur be financed and how is this developing? What sort of financing options should entrepreneurs – future high net worth individuals – consider, and what investment ideas should wealth advisors take seriously? To discuss these ideas is Joe Milam, who is founder of The Legacy Funds, which is a “franchise-like” venture-as-a-service platform, enabling local licensee/general partners to use the technology, back-office, company-specific and portfolio analytics and QSBS tax optimization, which is built into the firm’s platform, to solve the funding gaps.

The editors of this news service are pleased to share these views with readers; but do not necessarily share all contributors’ views and invite readers to respond. Email the editor at tom.burroughes@wealthbriefing.com

Introduction

To analyze the ineffectiveness of the current model of venture

capital and explore some initiatives to improve it, this essay

will briefly review the current state of venture investing, what

the future of entrepreneurial finance could look like, and the

barriers to change. Entrepreneurs need and investors want a more

efficient path to capital, closer to home.

To achieve this, impact investors should consider the well-tested methods of the public market for the venture class, including standardized reporting, portfolio structure, and tax optimization, specifically in underserved areas outside of the traditional VC regions.

The problem: entrepreneurs need better solutions and

investors want more

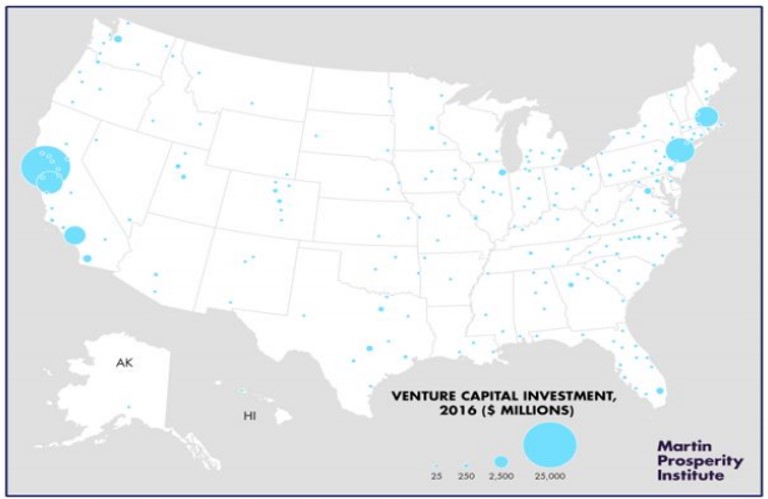

Although entrepreneurial activity is spreading outside Silicon

Valley, funding for startups continues to be concentrated in few

entrepreneurial communities. Investors are funding larger rounds

in later stage companies, with over 70 per cent of total dollars

committed in just two regions: the West and Mid-Atlantic.

Total dollars invested continues to rise but the number of companies getting funded is declining, with first-time funding flat compared to levels 5 years ago. Entrepreneurs struggle to source early stage capital and those that reach escape velocity and need substantial growth capital, often source it from - and move to - the coasts.

While we have expanding entrepreneurism, we see concentrated investing. Investors have acknowledged this concentration and many are exploring ways to support economic vibrancy in outside communities. Investing in early stage private companies that not only offer the prospect of positive financial results, but are delivering products or services that will benefit an underserved market has been labeled place-based impact investing.

The expectations of the wealthiest families to invest their capital in a manner consistent with their values, generalized in the public markets as the environment, sustainability and governance (ESG) standards or the 17 Sustainable Development Goals for public and private market investments, has had a material impact on the flow of capital. According to the 2018 GIIN Annual Impact Investor survey, the 226 respondents manage more than $228 billion in impact investing assets. Capital is available but is it moving efficiently? Some analysis reports as little as 15 per cent of all venture funds deliver alpha over any rolling 10-year period relative to the Russell 3000. The poor performance alone substantiates the need to bring innovation to the venture model.

The Kauffman Foundation’s findings from a 2012 analysis are in agreement. The foundation is an active venture investor within the assets of the foundation (approximately $1.7 billion at the time). The returns of their venture investing activity over the prior 20 years sheds some objective light on the actual returns of the asset class.

We conducted significant historical performance analyses of our venture capital portfolio and the results show chronically disappointing returns over most of the 20 years studied, no matter which way we slice the performance data – IRRs (internal rates of return), investment multiples, or PME (private market equivalents). This was a surprising and unexpected conclusion. As recently as 2009, we reported our comparative performance to our investment committee as evaluated against fund-of-fund returns provided by Cambridge Associates. It showed the Kauffman PE portfolio (including both VC and buyouts) to be in the “top quartile” of such investors.

Further, the absence of consistent and standardized reporting similar to the public market is a source of inefficient markets, rent-seeking behavior, and perpetuates the high cost of equity. Imagine if there were not the GAAP accounting standards and SEC-mandated reporting expectations. Investors would be beholden to the opinions of individuals and firms claiming an information advantage on individual companies.

Barriers to change

Any systematic change is met with resistance. Creation of funds

like these are possible but investors and startups alike are

wary. Entrepreneurs are busy and reporting takes time. Career

investors have their own processes and questions to determine a

venture’s progress and trajectory.

The call for change is evidenced in a recent Forbes article, reporting that just 56 per cent of Americans say they have a positive image of capitalism and the idea itself could be reimagined as authentic, accessible, and accountable. The Economic Innovation Group makes a case for the urgency of change with their New Map of Economic Growth, with analysis suggesting that gains from growth have and will continue to consolidate in the largest and most dynamic areas and leave other areas searching for their place, essentially compounding the current uneven concentration of opportunity and wealth.

Soon, American Millennials will account for a large section of the workforce, socially and culturally primed for entrepreneurship. It’s important that the system works in their favor, whether they are in Silicon Valley or not.

What the future of entrepreneurial finance could look

like

Startups and investors alike should be rewarded for their efforts

to do the right thing, for the right reasons.

Investors would have:

-- Access to a venture fund that genuinely managed

portfolio risk using institutionally rigorous diversification and

security selection strategies;

-- Confidence that the fund was optimizing tax laws

1202 and 1244 that could lower the after-tax risks, and make any

profits potentially tax free, and adequately report those

implications;

-- Complete transparency into such portfolio and

fund, such that if an investor wanted to invest additional

capital into a particular company, they could; and

-- Geographic focus, such that the investors’

interest in place-based impact investing could be served.

Entrepreneurs would provide:

-- Standardized operating information

consistently;

-- Be rewarded for their transparency with easier access to

initial and follow-on funding; and

-- Spend less time pitching to investors, allowing more

time to focus on their business.

In an index-like fund with meritocratic incentives, startups would qualify for a predetermined amount of funding, with investors reserving additional capital for future funding. The fund would more closely resemble the likes of portfolio management firms, with a wide array of companies (regardless of industry) participating. The only commonality would be geography, keeping innovation close to home.

The need is clear

The need to mobilize more capital into more regions, and a more

diverse population of entrepreneurial ventures, is clear. The

Opportunity Zones incentives, passed in 2017 as part of the Tax

Reform Act of 2017, is evidence.

There also needs to be better distribution of the economic benefits of capitalism, as has been covered in other publications as well. The concentration of wealth, at the expense of the middle class, is also well documented.

Simply stated, more people, in more regions of the country, need to participate in the economic mobility and self-determination as availed through small business and entrepreneurial activities.

The existing funding mechanisms - and incentives – must change. Thankfully, professional investing structure and practices are arriving at the venture asset class. It’s about time.

Funding entrepreneurial activity needed to grow up.